For the past few years, the central narrative that investors and analysts have used to weave the market and economy’s movements into a single, cohesive thread is the coronavirus.

While just about everybody wants to relegate the pandemic to history, its effects are still having an impact on daily life, and on the market. Variants of the virus sparked multiple infection waves through 2021 that kept hospitalizations high and strained the health care system in general. As 2022 started, some of those effects seemed to have tapered enough that the narrative began to shift its focus to questions about the pace of inflation and the increases in interest rates that have come as a result. The colder months that ended 2022 and started 2023 in the U.S. brought warnings about new spikes as the virus continues to mutate.

For most of the past year, the COVID discussion has taken a back seat to questions about inflation, interest rates, and the global issues that continue to keep the market on edge. While news and global attention is focused elsewhere, the pandemic isn’t going away. Even while local and national governments have moved to endemic-phase monitoring and management, the fact remains that the risk of new variants can’t be entirely dismissed. I believe that means that research into the long-term efficacy of current vaccines will be an ongoing concern, with continued emphasis on encouraging vaccinations and booster shots. The flip side of that argument comes from recent reports from the largest producers of COVID vaccines and antiviral treatments about rapidly declining demand.

One of those companies is Pflizer Inc. (PFE). They were among the leaders in the global effort to develop, deliver and administer vaccines around the globe. In 2021 and even most of last year, sales of their vaccine as well as their antiviral treatment (Paxlovid) propelled sales to record levels. After the company’s latest report, however, management predicted sales of its COVID products to drop by about 31% this year. That news accelerated a drawdown in the stock’s price that begin in December and now has the stock trading at around $40 per share.

It’s worth pointing out that vaccines are just one part of a diversified pharmaceutical company’s development pipeline. As one of the leading pharmaceutical companies in the industry, PFE boasts a broad portfolio with eight separate drug brands that each account for more than $1 billion in annual sales, but none that contribute more than 14% of total revenue. They also have a large development pipeline, especially as already mentioned in oncology drugs where most analysts see strong long-term growth that should offset the effect of increased competition in existing brands as patent protections expire and biosimilar and generic drugs start to take up market share.

The company’s leading position in its industry, along with the massive windfall over the last two years from sales of its COVID vaccine have put PFE on solid fundamental footing. Does that suggest that the stock’s big drop could really just be a useful opportunity for long-term, value-oriented investors? Let’s find out.

Fundamental and Value Profile

Pfizer Inc. (Pfizer) is a research-based global biopharmaceutical company. The Company is engaged in the discovery, development and manufacture of healthcare products. Its global portfolio includes medicines and vaccines, as well as consumer healthcare products. The Company manages its commercial operations through two business segments: Pfizer Innovative Health (IH) and Pfizer Essential Health (EH). IH focuses on developing and commercializing medicines and vaccines, as well as products for consumer healthcare. IH therapeutic areas include internal medicine, vaccines, oncology, inflammation and immunology, rare diseases and consumer healthcare. EH includes legacy brands, branded generics, generic sterile injectable products, biosimilars and infusion systems. EH also includes a research and development (R&D) organization, as well as its contract manufacturing business. Its brands include Prevnar 13, Xeljanz, Eliquis, Lipitor, Celebrex, Pristiq and Viagra. PFE has a current market cap of $277.6 billion.

Earnings and Sales Growth: Over the last twelve months, earnings increased by 5.5%, while revenues increased by about 1.9%. In the last quarter, earnings decreased by nearly -36% while sales were 7.3% higher. The company’s margin profile is healthy, but showing signs of weakness; over the last twelve months, Net Income as a percentage of Revenues was 31.27%, but declined sharply, to a little more than 20.5% in the last quarter.

Free Cash Flow: PFE’s free cash flow is very strong, at more than $26 billion over the last twelve months. That does mark a decline from about $31 billion a year ago, but also increased from $23.3 billion in the last quarter. The current number translates to a Free Cash Flow Yield of 11.43%.

Debt to Equity: PFE’s debt to equity is .34, which is a conservative number. The company’s balance sheet indicates that operating profits are more than adequate to service their debt, with healthy liquidity to provide additional flexibility. Cash and liquid assets were about $22.7 billion in the last quarter (down sharply from $36.1 billion in the quarter prior), while long-term debt was $32.8 billion – down from $49.7 billion at the beginning of 2021.

Dividend: PFE’s annual divided is $1.64 per share, and which translates to a yield of about 4.04% at the stock’s current price. It is also noteworthy that the dividend increased at the beginning of 2020 from $1.52 per share, from $1.56 in mid-2021, and $1.60 prior to the latest earnings announcement. An increasing dividend is a useful indication of management’s confidence in their approach.

Price/Book Ratio: there are a lot of ways to measure how much a stock should be worth; but I like to work with a combination of Price/Book and Price/Cash Flow analysis. Together, these measurements provide a long-term, fair value target at around $51.50 per share. That means that PFE is modestly undervalued right now, by about 27%.

Technical Profile

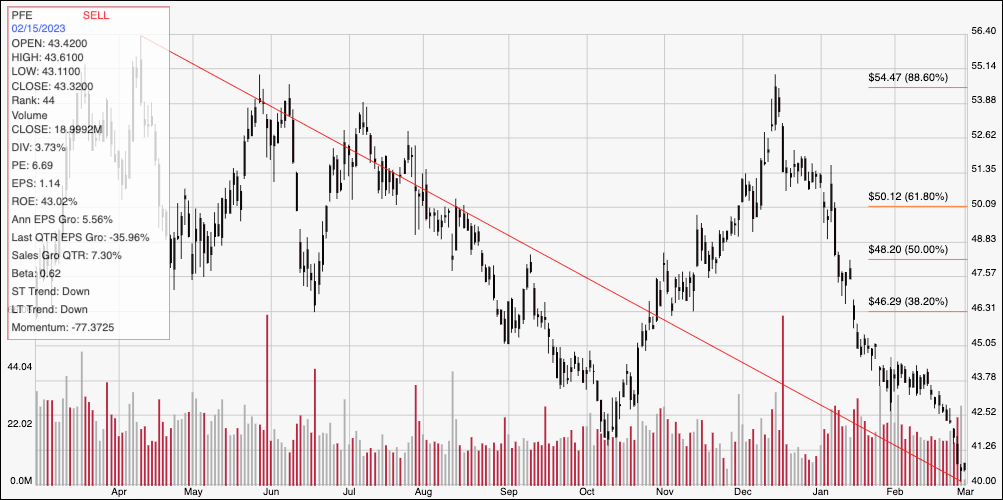

Here’s a look at the stock’s latest technical chart.

Current Price Action/Trends and Pivots: The chart above covers the last year of price activity. The red diagonal line traces the stock’s downward trend from its March 2022 high at around $56.50 to its current price which marks its latest 52-week low at around $40 per share. It also provides the baseline for the Fibonacci retracement lines shown on the right side of the chart. The stock has been declining since a December peak at around $54, and has extended that downward trend over the last couple of weeks after a temporary stabilization period at around $45. Current support is at about $40, with immediate resistance at about $42 based on a pivot low in mid-October of last year. A push above $42 should find next resistance at about $44, while a drop below $40 would be expected to find next support at around $38, using the current distance between support and resistance as a reference point.

Near-term Keys: PFE’s balance sheet has nearly “fortress”-level strength, even with the latest drop in cash, with robust, rising free cash flow to provide additional stability and growth potential. The current decline in net income and cash is a concern, as they do reflect what I attribute as rising input costs that continue to impact every sector of the economy; however PFE has a lot of flexibility to work with and better ability than most companies to ride through the difficulty. PFE’s value proposition is interesting, and certainly enough to make the stock something to consider using right now for a long-term investing opportunity – but keep in mind that the current, clear bearish momentum implies additional downside risk below the stock’s current price. If you prefer to focus on short-term trading strategies, buying call options or the stock outright would be a very speculative trade; however, you could use a push above $42 as a signal to consider buying the stock or working with call options, using a bullish near-term target price at around $44 to take profits. You could also use a drop below $40 as an opportunity to think about shorting the stock or buying put options, using $38 as a practical bearish target.