If you pay attention to the stock market, you inevitably become familiar with some of the personalities that take up space on market media to talk about it.

On CNBC, for example, Jim Cramer is an ever-present commentator. Not only does he host his own “Mad Money” show in the afternoons on the network, you’ll also find him on the floor of the New York Stock Exchange each morning during the “Squawk on the Street” segment. He’s been a TV personality since 2005, when “Mad Money” first began airing.

What’s the draw for the average investor to somebody like Cramer? He’s well educated, and a veteran of the stock market. As the manager of his own hedge fund from 1988 to 2000, he was hugely successful, posting just a single year of negative returns and finally retiring the fund in 2001 with average annual returns of 24%. He’s opinionated, energetic, and sometimes frenetic on-screen, which can be pretty entertaining at times.

His opinions about individual stocks carry some weight with the average investor, but as with most “talking heads,” I’ve found over time that it’s usually smart to take his opinions with a grain of salt. It’s true that I’ve been able to use some of his commentary as a starting point for my own analysis; but at the same time, Mr. Cramer is also one of the big reasons that I have come to believe that by the time I hear about a stock in the news, most of the opportunity in the stock has already passed the rest of us by.

Not long ago, Mr. Cramer gave me a good reminder of the value of paying attention to market news, as well as the need to leaven “talking head” opinions with my own analysis. In talking about the challenges that took down the entire Tech sector in 2022, for example, Mr. Cramer dismissed several of the most well-known and established names, but suggested that semiconductor stock Marvell Technology (MRVL) may be a good value pick. I’ll admit, that initially piqued my interest, which prompted me to take a closer look through the company’s fundamental strength as well as its latest price action to determine if the stock might offer a useful, new investing opportunity.

Like most Tech stocks, MRVL has been following a long-term downward trend for the past year, falling from a January 2022 peak at around $92 to a trend low at around $34at the beginning of this year. After staging a temporary rally to about $49 at the start of February, the stock dropped back again and appears to be settling into a narrow consolidation range in the low $40 range. What do the company’s latest fundamentals say about the stock’s value proposition? Does that consolidation range suggest a useful bargain opportunity could be had? Let’s dive in and look at the numbers.

Fundamental and Value Profile

Marvell Technology, Inc., through its subsidiaries, is a supplier of infrastructure semiconductor solutions. The Company is engaged in the design, development and sale of integrated circuits. Its product solutions serve five markets, such as data center, carrier infrastructure, enterprise networking, consumer, and automotive/industrial. Its product offerings include custom application-specific integrated circuits (ASICs), electro-optics, Ethernet solutions, fiber channel adapters, processors and storage controllers. It develops custom system-on-a-chip (SoC) solutions tailored to individual customer specifications. Its electro-optical products include pulse amplitude modulation (PAM) and coherent digital signal processors (DSPs), laser drivers, trans-impedance amplifiers (TIAs), silicon photonics and data center interconnect (DCI) solutions. It offers a portfolio of Ethernet solutions spanning controllers, network adapters, physical transceivers and switches. MRVL has a market cap of $36 billion.

Earnings and Sales Growth: Over the last twelve months, earnings decreased by almost -3%, while sales increased about 5.6%. In the last quarter, earnings fell -17%, while sales declined by -7.73%. The company’s operating profile is showing a potential reversal of some of the cost pressures that I think have affected the entire sector throughout the past year or so. Over the last twelve months, Net Income was -2.76% of Revenues, and improved in the last quarter to -1.09%. The improvement is interesting, and could be a positive sign, however additional improvement in the quarters ahead is needed to provide confirmation of this positive pattern.

Free Cash Flow: MRVL’s free cash flow is modest, at about $1.08 billion over the last twelve months. It does mark a useful increase over the past year, from $843.1 million. The current number translates to a Free Cash Flow Yield of 3.02%.

Debt to Equity: MRVL has a debt/equity ratio of .25. This is a conservative number that reflects a conservative approach to leverage. The company’s balance sheet shows $911 million in cash and liquid assets in the last quarter (rising from $723.4 million in the last quarter, and $465 million a year ago) versus about $3.9 billion in long-term debt. While operating margins negative, their cash and positive, increasing free cash flow are good indications that servicing their debt isn’t a problem. Even so, a reversal of MRVL’s current operating margins would provide additional evidence of the company’s solid footing.

Dividend: MRVL pays an annual dividend of $.24 per share. At the stock’s current price, that translates to minimal dividend yield of about .57%. Considering that few stocks in the Tech sector pay a dividend, however, management’s commitment to return value via dividend distributions is a positive sign of fundamental strength.

Price/Book Ratio: there are a lot of ways to measure how much a stock should be worth; but I like to work with a combination of Price/Book and Price/Cash Flow analysis. Together, these measurements provide a long-term, fair value target at around $56 per share. That means the stock is significantly undervalued, with about 33% upside from the stock’s current price.

Technical Profile

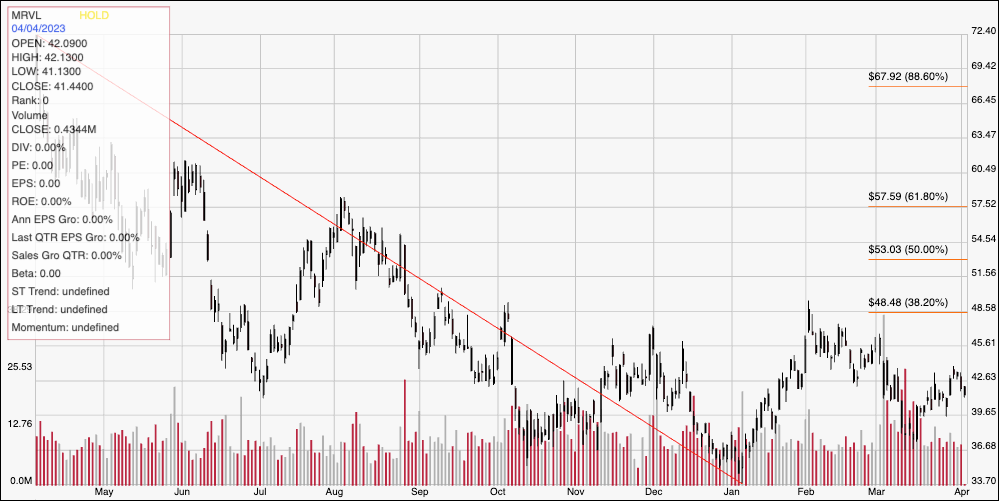

Here’s a look at MRVL’s latest technical chart.

Current Price Action/Trends and Pivots: The chart above clearly shows the stock’s downward trend over the past year, from an April peak at around $72.50 to its low, reached at the beginning of this year at around $34. That downward trend also provides the reference for the Fibonacci retracement lines shown on the right side of the chart. After rallying to about $48.50 in February, the stock slipped back again to find a new pivot low at around $37 in March before starting a new push up to the stock’s current price at around $41. Current support is around $39.50 based on the most recent pivot low, with immediate resistance at around $43 where the stock hit a pivot high last week. A push above $43 should have initial upside to about $45.50, with $48.50 reachable if buying activity increases. A drop below $39.50 should find next support at around $37, with a retest of the stock’s yearly low at around $34 possible if bearish sentiment increases.

Near-term Keys: MRVL is a company with an interesting set of fundamentals that could be signaling to improving strength, along with a value proposition that is very tempting at the stock’s current price. I do believe there is additional downside risk for the entire sector under current economic conditions, which means that using this stock as a useful long-term opportunity implies you should also accept that additional downside risk in the nearer term. If you prefer to work with short-term trading strategies, a push above immediate resistance at $43 could be a signal to consider buying the stock or working with call options, using $45.50 as an initial exit target, and $48.50 if buying momentum increases. A drop below $39.50 would be a good signal to think about shorting the stock or buying put options, with a useful bearish profit target at around $37, and $34 possible if selling activity increases.