One of the best tools I’ve found to filter through the market quickly for fundamental strength is dividend payout.

Dividends are one of the simplest ways for a company’s management to express confidence in its long-term prospects, and to return value to its shareholders. Talking heads and a lot of analysts tend to focus on stock repurchases, but I think dividends are better, because they act as a passive income source that puts useful, periodic cash in shareholder’s accounts.

The economic conditions of the last three years have only reinforced the value of dividends as a fundamental metric in my system. That’s because a lot of companies chose to reduce or eliminate their dividend payouts altogether as a way to preserve cash to weather the difficult conditions imposed by COVID restrictions in 2020. While understandable, it also provided a refined method to filter quickly through the market and identify the stocks that are likely to provide the best fit for my preferred investing method. The fact that a lot of stocks also dropped to or near historical lows during that time helped as well, as valuations across the board improved.

Since the end of 2021, economic and social activity has begun to return to some form of normal. That is a big part of what spurred economic growth to the point that in 2022 the Fed began raising interest rates aggressively, so that now in 2023 the question is no longer how long rates will remain high, but whether those increases will aid the “soft landing” the Fed is aiming for, or simply push the economy into a complete, new recession. The effect of that uncertainty for most of the last year has been volatility that pushed the market into its own legitimate bear market in 2022, and has kept the market on uneven footing throughout the first quarter of 2023. To me, that implies that a lot of companies that have dropped to attractive valuation levels may remain low, or even move lower this year. That means that dividends will continue to be a useful way to filter the market for stocks that I think provide the best opportunities to keep your money working for you.

One example of a stock that announced a resumption of dividend payments in 2022 is Cal-Maine Foods, Inc. (CALM). This is a company in the defensively positioned Food Products industry of the Consumer Staples sector that has historically followed a variable dividend payout policy, based primarily on whether it achieves a positive Net income result in a given quarter. In 2021, management announced a $.034 per share dividend payout, followed by a $.13 per share payout in the first quarter of 2022, $.85 for their last payout of the year, and $1.35 a quarter ago, and a new payout of $2.20 per share date following their most recent earnings announcement. The resumption of its dividend, along with the increases implemented over the past year are positive marks for the company’s generally improving fundamental picture.

This is also a stock that has diverged from the pattern of the broad market, and even many stocks in the Food Products industry most of the past year. From a low point at around $34 in January of 2022, the stock peak in December at around $65.50, marking an impressive upward trend for the year. Since then, the stock dropped back to find a new stabilization level at around $52. Following a temporary, mid-February rally to about $61.50, the stock followed broader market momentum through most of March lower before rallying back to that $61.50 high immediately after the latest earnings data was released. Volatility in the last three days has pushed the stock back down again, putting it its current price at around $56 per share. Fundamentally, the company an improving fundamental profile, with improving margins, free cash flow, and liquidity. Along with its current price action, the stock could be sitting at a level that makes it useful as a long-term, defensive investment during uncertain market conditions. Let’s dive in.

Fundamental and Value Profile

Cal-Maine Foods, Inc. is a producer and marketer of shell eggs in the United States. The Company operates through the segment of production, grading, packaging, marketing and distribution of shell eggs. It offers shell eggs, including specialty and non-specialty eggs. It classifies cage free, organic and brown eggs as specialty products. It classifies all other shell eggs as non-specialty products. The Company markets its specialty shell eggs under the brands, including Egg-Land’s Best, Land O’ Lakes, Farmhouse and 4-Grain. The Company, through Egg-Land’s Best, Inc. (EB), produces, markets and distributes Egg-Land’s Best and Land O’ Lakes branded eggs. It markets cage-free eggs under its Farmhouse brand and distributes them throughout southeast and southwest regions of the United States. It markets organic, wholesome, cage-free, vegetarian and omega-3 eggs under its 4-Grain brand. It also produces, markets and distributes private label specialty shell eggs to customers. CALM has a current market cap of about $2.7 billion.

Earnings and Sales Growth: Over the last twelve months, earnings grew by more than 717% (not a typo), while revenues increased by nearly 109%. In the last quarter, earnings were 62.65% higher, while sales rose by more than 24.42%. The company’s margin profile has recovered from a negative pattern that predated the pandemic, and has been showing robust strength for the last couple of quarters. Net Income as a percentage of Revenues over the last twelve months was 24.82%, and strengthened to 32.4% in the last quarter.

Free Cash Flow: CALM’s free cash flow is very healthy, at almost $705 million; that is a continuation of a strengthening trend from negative Free Cash Flow of -$32 million a little over a year ago, and $386 million in the prior quarter. The current number translates to a very strong Free Cash Flow Yield of 25.34%.

Debt to Equity: CALM’s debt to equity is .0, which means that CALM has no long-term debt. Their balance sheet shows a little more than $645 million in cash and liquid assets. CALM has healthy, improving liquidity; a little over a year ago, their balance sheet showed just a little over $96 million in cash, and $279.35 million in the quarter prior to the most recent earnings report.

Dividend: CALM’s dividend payouts so far in 2022, if followed consistently over time, work out to an annualized dividend of about $5.15 per share. I qualify that metric because CALM has historically kept their dividend variable, and can be expected to continue to do so. As previously mentioned, management has been increasing their dividend consistently for the past year, which is a positive signal.

Price/Book Ratio: there are a lot of ways to measure how much a stock should be worth; but I like to worth with a combination of Price/Book and Price/Cash Flow analysis. Together, these measurements provide a long-term target at around $79 per share. That suggests CALM is undervalued by about nearly 40% right now. It is also worth noting that as of the last quarter, this same analysis yielded a fair value target price at around $68.50 per share.

Technical Profile

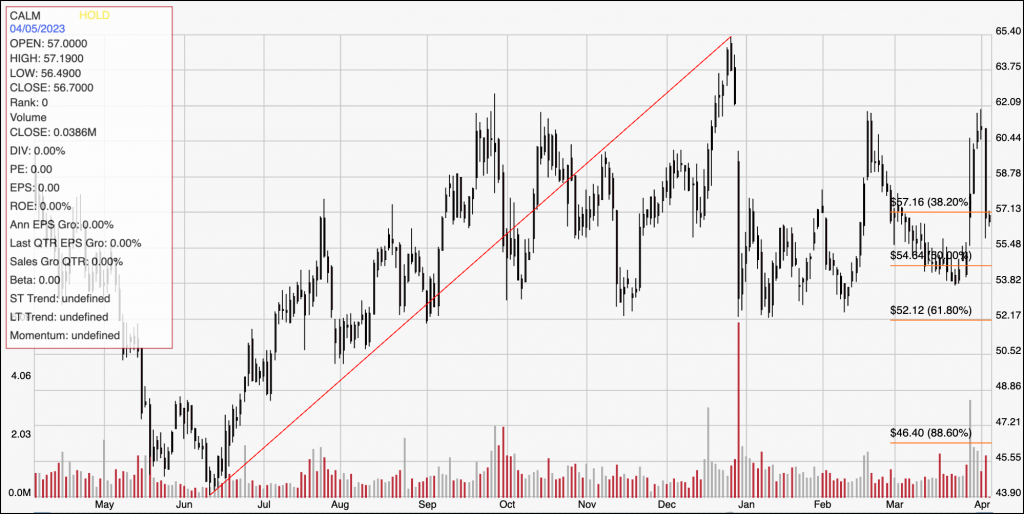

Here’s a look at the stock’s latest technical chart.

Current Price Action/Trends and Pivots: The diagonal red line traces the stock’s upward trend from a June 2022 low at around $44 to its December high at about $65.50. It also provides the reference for the Fibonacci retracement lines on the right side of the chart. From its February peak at around $61.50, the stock dropped sharply, finding major support right around the 61.8% retracement line in the $52 price area. After staging two temporary rallies to about $61.50 in February and again at the end of March, the stock has dropped to about $56, a little below the 38.2% retracement line, to mark immediate resistance at around $57, with current support at around $54 based on the most recent pivot low point. A push above $57 should find next resistance at around $61.50. A drop below $54 should find secondary support at around $52, based on pivot lows in January as well as the 61.8% retracement line.

Near-term Keys: The stock’s recent drop off of its latest high could be setting up an interesting signal to “buy the dip”, which means that a push above $57 could be an interesting signal to consider buying the stock or working with call options, with $61.50 acting as a useful profit target on a bullish trade. A drop below $54 could be a signal to consider shorting the stock or buying put options, with $52 providing a practical bearish profit target. The stock’s fundamental strength and value proposition, in the meantime remains attractive under current market conditions, and in fact has gotten even better since the last earning report. If you don’t mind the fact this stock does demonstrate characteristics of volatility, it could be worth taking seriously right now as a useful long-term opportunity.