One of the sectors of the economy that I’ve learned to follow over the course of my investing career is the Energy sector.

This is a sector that has a broad carryover effect on multiple other sectors in the economy, which is why I have learned that it’s useful to pay attention to the price of crude oil and other energy commodities, like natural gas on the global market. Despite increasing attention on things like electric vehicles, “green” technologies and solutions aimed at reducing carbon footprints, the plain and simple fact of the matter is that oil continues to be a key driver of economic stability all over the world. That even applies to the production of the material assets used in “green” technologies like electrical car batteries and solar panels, to name just a couple of simple examples. Oil and natural gas liquids (NGLs) are also used in a variety of other petrochemical applications and industries including plastics, home building, fertilizers, and pharmaceuticals. It also means that when events threaten the stability of supply and price, the ripple effect could extend into just about every part of the global economy.

Over the last decade, shale oil exploration and production have helped the U.S. narrow the gap between western and Brent (mostly oil from the Middle East) and WTI (the generalized benchmark for U.S. oil) crude production, with a major portion of shale oil coming from the Permian Basin of the southwestern part of the United States. The challenge associated with U.S. production – and one of the things that contributed to keep oil prices relatively low prior to the COVID-19 pandemic – is that exploration and production of shale oil exceeded the capacity of midstream companies to transport the oil to its primary distribution centers before it is sold throughout the world.

Midstream oil companies include those that are involved in the ongoing construction, operation, and maintenance of pipelines and storage facilities out of the areas of the U.S. that drive shale production, like the Permian Basin. Limitations of existing pipeline and storage capacity have been the primary reason that inventory out of that area in particular remained stuck in the Basin through 2019 and kept the entire industry waiting for new pipeline projects to be completed. Many of those projects were delayed in 2020 because of the pandemic, but have since been completed, alleviating one concern about supply even as other headwinds arose – in particular, the effect of inflation and rising interest rates on production. That, along with production cuts from OPEC-participating countries and policies from the current U.S. presidential administration that heavily favors “green” energy solutions over traditional oil commodities, have kept oil prices elevated for most of the past two years.

Enterprise Products Partners (EPD) is one of the biggest midstream companies with operations in crude oil, natural gas and liquified natural gas (LNG) transport and storage, among other things. EPD isn’t an easily recognizable company by name, but it is well-established and recognized among its peers, with a very interesting fundamental profile that includes a large dividend and critical fundamental metrics like free cash flow that have seen significant improvements over the past year. EPD’s management has also noted that operating margins ticked higher in 2021, driven primarily by strong export demand for natural gas liquids logistics and consumer-led demand for petrochemicals such as cleaning products and a built a useful backlog of pending orders that are expected to provide continue to provide a good tailwind as previously suspended or deferred projects are carefully and deliberately brought back into production to keep pace with demand. Another element that I expect will work in this company’s favor is its presence in the transportation systems used for LNG in the United States. With Russian energy exports being severely restricted in response to its war against Ukraine, demand for regionally produced LNG products should also remain high.

Over the last year, oil prices have tumbled from a peak at above $120 to a current level at around $72, putting a lot of pressure on the entire sector. For EPD, that’s kept the stock’s price between $23 and $29 per share. In 2023, the stock has managed a counter-market upward trend that has the stock a little 8% its January starting point. I think that, on a very selective basis, energy stocks continue to provide many of the best values in the marketplace, with commodity price support that should make these stocks more resilient than many other industries under current economic conditions. What about EPD? Are its fundamentals strong enough to mark it as a useful value as well? Let’s find out.

Fundamental and Value Profile

Enterprise Products Partners L.P. (Enterprise) is a provider of midstream energy services to producers and consumers of natural gas, natural gas liquids (NGLs), crude oil, petrochemicals and refined products in North America. The Company’s segments include NGL Pipelines & Services; Crude Oil Pipelines & Services; Natural Gas Pipelines & Services, and Petrochemical & Refined Products Services. The Company’s midstream energy operations include natural gas gathering, treating, processing, transportation and storage; NGL transportation, fractionation, storage, and import and export terminals, including liquefied petroleum gas (LPG); crude oil gathering, transportation, storage and terminals; petrochemical and refined products transportation, storage, export and import terminals, and related services, and a marine transportation business that operates primarily on the United States inland and Intracoastal Waterway systems. EPD has a current market cap of about $56.8 billion.

Earnings and Sales Growth: Over the last twelve months, earnings increased by a little more than 6.67%, while revenues were -4.34% lower. In the last quarter, earnings decreased by -1.54%, while sales were -8.84% lower. The company’s margin profile is healthy; in the last quarter, Net Income as a percentage of Revenues in the last quarter was 11.18%, which increased from 9.69% over the last twelve months.

Free Cash Flow: EPD’s free cash flow is healthy, at a little more than $5.3 billion over the last twelve months. That does mark a decline from about $6.2 billion in the quarter prior and $7.1 billion a year ago. The current number also translates to a Free Cash Flow Yield of 9.38%.

Debt to Equity: EPD’s debt to equity is 0.98, which is a little higher than I prefer to see, but also isn’t unusual for stocks in this industry; however the company’s margin profile indicates operating profits should be adequate to service their debt. Their balance sheet has been a bit of a concern, as liquidity has been limited in the last quarter. The company reported $276 million in cash and liquid assets versus $27.4 billion in long-term debt, with no major near-term debt obligations. About a year and a half ago, cash and liquid assets were more than $2.9 billion, with a major drop below $500 million a little over a year ago that has continued to the latest report. Their operating margins, along with healthy and growing free cash flow suggest that debt service isn’t a problem, however the drop in liquidity remains a source of concern as the company’s normally healthy financial flexibility becomes more and more restricted.

Dividend: EPD’s annual divided is $1.96 per share, which translates to a much larger-than-normal yield of about 7.52% at the stock’s current price. A number of other companies in the Energy sector have been forced to reduce or even eliminate dividend payments, so EPD’s ability to maintain their attractive dividend and even increase it (from $1.80 at the start of 2022, and $1.90 at the start of this year) is a sign of management’s confidence.

Price/Book Ratio: there are a lot of ways to measure how much a stock should be worth; but I like to work with a combination of Price/Book and Price/Cash Flow analysis. Together, these measurements provide a long-term, fair value target at around $27 per share. That means that the stock is pretty fairly valued, with about 4% upside from its current price, and a practical discount price at around $21.50. It is also worth noting that in 2022, this same analysis yielded a fair value target at around $31.50 per share.

Technical Profile

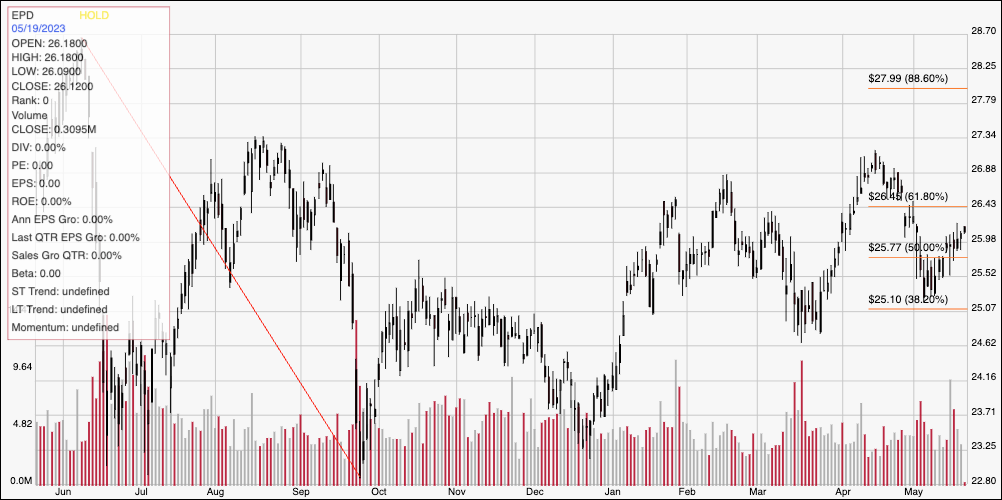

Here’s a look at the stock’s latest technical chart.

Current Price Action/Trends and Pivots: The chart above covers the last year of price activity. The red diagonal line traces the stock’s decline from about $29 in June of last year to its low in September at about $23. It also informs the Fibonacci retracement lines shown on the right side of the chart. The stock has staged a gradual upward trend from that point, with the stock fading off of the latest high near $27 in April and rebounding off of major trend support at around $25, roughly where the 38.2% retracement line sits in the early part of this month. The stock’s bullish momentum from that point recently pushed the stock above latest resistance, putting current support at around $25.50, with immediate resistance expected at around $26.50, where the 61.8% retracement line waits. A push above $26.50 will find additional resistance at around $27.50, where the stock peaked in August, but could rally to about $28 if bullish momentum persists. A drop below $25.50 should have limited downside, with next support expected to sit around $25 where the 38.2% retracement line rests.

Near-term Keys: EPD’s fundamental strength remains generally solid, however the latest declines in Free Cash Flow, along with increasingly limited cash are reasons to accept that the stock doesn’t offer a useful value proposition right now. Its high, increasing dividend offers an interesting argument for the stock as a useful long-term buy-and-hold position, however I would wait to see improvements in these other metrics first. If you prefer short-term trading strategies, a push above $26.50 could be an interesting signal to buy the stock or work with call options, using $27.50 to $28 as a useful bullish profit target. The stock’s current upward trend, and limited downside don’t provide a lot of great signals to use for a bearish trade, so shorting the stock or buying put options would be a very speculative, low-probability strategy without enough reward to justify it.